Capital Part of Indian Budget

Points to Ponder in This Article – Understand what constitutes the capital part of the Indian budget. With time government makes certain changes like planned and non-planned expenditure has been done away with from 2017 from the annual financial statement, targets of FRBM act are constantly in question & are debated to change into a range rather than a fix value. Hence, just understand what comes under the capital part of Indian budget system.

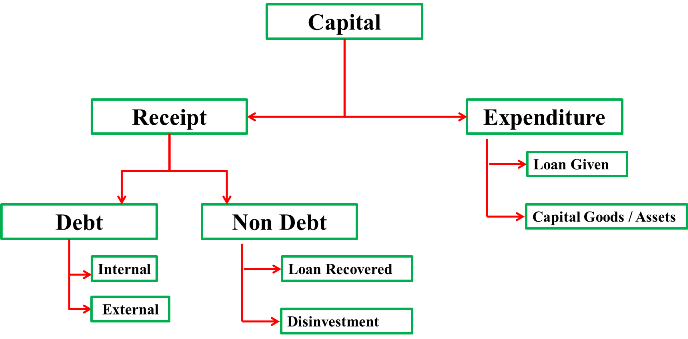

Capital Budget consists of capital receipts (like borrowing, disinvestment) and long period capital expenditure (creation of assets, investment). Capital receipts are receipts of the government which create liabilities or reduce financial assets, e.g., market borrowing, recovery of loan, etc. Capital expenditure is the expenditure of the government which either creates assets or reduces liability.

Capital Receipt |

Capital Expenditure |

Debt

Non-Debt

|

|

- Disinvestment matter falls under Department of Disinvestment under Finance minister.

- Within Capital Receipt → Debt Internal > External

- Within capital Expenditure → Five year plans > Defense > loans (PSU, State, UT)

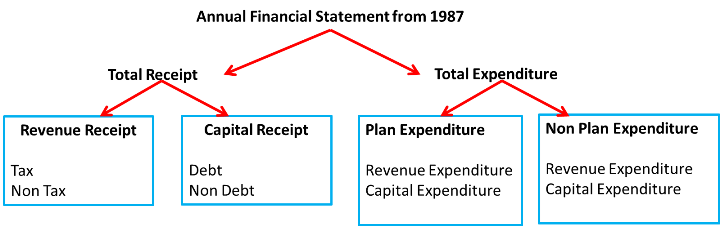

Annual Financial Statement format changed in 1987

| Total Income | |||

| Revenue (Receipt) | Capital (Receipt) | ||

| Tax | Non-tax | Debt | Non Debt |

|

|

|

|

| Total Expenditure | |

Plan Expenditure (Revenue + capital)

|

Non plan Expenditure (Revenue + capital)

|

| Non plan Expenditure | |

| Revenue Expenditure | Capital Expenditure |

|

|

- Non plan expenditure > Plan expenditure

- Majority of government money goes into revenue Expenditure approx. 60% of total expenditure.

- Highest amount of Plan Expenditure goes to Gender Plans > Child Plans > SC Plans > ST Plans

- Within Non-merit goods subsidies Food > Fertilizer > Petro (Society pays → individual benefits)

Deficits in Government Budget & Financing

| Revenue Deficit | Revenue Expenditure – Revenue Receipt |

| Effective Revenue Deficit | Revenue deficit – Grants given to State/UT for creation of capital assets |

| Budget Deficit | Total expenditure – Total receipts = Revenue deficit + capital deficit |

| Fiscal Deficit | Budget deficit + Borrowing = (Total Expenditure – Total Receipts) + Borrowing |

| Primary Deficit | Fiscal deficit – Interest on previous loans |

- A falling level of primary deficit implies that new borrowings are being used to meet old debt liabilities.

- Hence decreasing primary deficit means the rise in interest payment → Bad for economy.

- Deficits Higher to Lower → FD > RD > ERD > PD > BD

Fiscal Responsibility and Budget Management (FRBM) Act targets to FM

| Effective Revenue deficit | Eliminate (0%) by 31/3/2015 |

| Fiscal deficit | Reduce it to 3% of GDP by 31/3/2017 |

Countervailing & Anti-Dumping Duty

Countervailing Duty: To encourage exports, government grants subsidy to exporters which results in decreased cost of production for them. Hence exports are able to export at cheaper rates. It largely affects producers of importing country. To counterbalance (countervail) this, importing countries impose duty on imported good to raise the price of subsidized product to offset it lower price.

Anti Dumping Duty: Dumping means exporting goods to other country in large quantity at a cheaper rate. In India, anti-dumping duty is recommended by the Union Ministry of Commerce while it is imposed by the Union Ministry of Finance. There are 2 types of dumping:

Price Dumping: selling goods in foreign country at price lower than the price of home country.

Cost Dumping: It means selling goods in foreign countries at a price lower than cost of production. It is aimed at wiping out the domestic producers from the market. It is also called Predatory dumping.

- Duty imposed on dumped goods is called Anti-Dumping duty

- Countervailing duty is to counter the low cost of products due to subsidy while Anti-Dumping duty is to offset voluntary low price to capture the market.