Capital Market – Types of Bonds

Points to Ponder in This Article – Understand the different types of instruments that are used to raise money from the market. Understand the difference between different types of bonds which are oftenly used in India.

Ways to raise money from Market

Equity by selling shares and debts by selling bonds are two of the most famous ways to raise money from the market.

| Borrow Money (Debt) |

|

| Give Partnership (Equity) |

|

Debt Types

- Bonds, Debentures, Loans, ECB, T-Bills, Commercial Papers, Certificate of deposits

- Creditor to company & First claim during liquidation

- Yield (rate of return) and the maturity always inversely related

Bonds

- Carry fixed interest payable every year by the company

- For e.g. To whoever pays me Rs. 1000, I’ll pay annual 10% interest rate (Rs. 100)

- And after 5 years, I’ll also repay the principle amount Rs. 1000

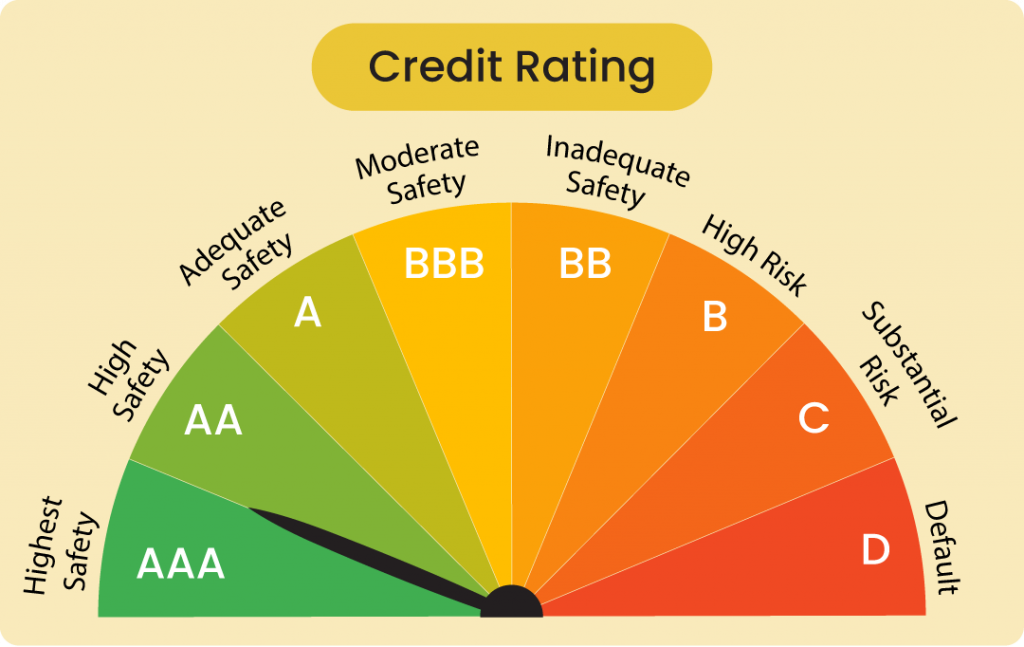

- SEBI Rule > If bond maturity > 18 months then getting credit rating is mandatory

Junk Bonds (High Yield Bond)

- Credit rating companies like CRISIL, S&P, Moody’s etc. give credit ratings (AA, A, BBB, C, D etc.) to a bond based on reliability & market value of a company

- If any Bond gets “C” or “D” rating, it means it is not creditworthy & may default on this loan; hence not much people will not invest in it.

- Hence to allure investors they provide various schemes or higher Interest rates on bands

- For e.g. “If you give me Rs. 1000, I’ll give you 25% interest rate per year”.

Also read: Capital Gains Tax, Transfer Pricing & GAAR

Gilt Edged Securities

- Government Securities & Treasury Bills (via RBI) & well-known companies with high credit ratings issues bonds

- High credit ratings assure an investor of its credibility & hence Gilt edged securities pay low rates generally 4% annually

Bearer Bonds

- Same as regular bonds, but don’t have “Holder’s Name” on them, instead have coupons attached with them.

- So, if anyone doesn’t want to withdraw the whole money, he can cut a few coupons and sell them to a broker to withdraw partial amount.

Bond Yield

- Bond yield to maturity > Total ROI of buyer on maturity

- If bond price decreases, Bond yield increases

- For ex. Bond value is Rs. 1000 for 10 % annually

- Hence initial bond yield is 10% for first investor

- If he sells it to second investor at Rs. 900 then his bond yield will be 10/900 > 11%

Factors deciding Bond Yield

- Assured return with good credit rating > Low bond yield

- Bankruptcy rumour in market for a company > panic sales by investors > Bond yield goes high

- Credit rating down > next time have to offer higher interest rate > Junk bond

Debt Instruments

- Credit rating . Gilt securities vs Junk bonds

- Bond vs Debenture

- Optionally fully convertible debentures (OFCD)

- Other types of Debentures

- Inflation indexed bonds (IIB)

Credit rating for Sovereign Bonds (Rating of Countries)

- Credit rating companies like CRISIL, S&P, Moody’s etc. also give credit ratings (AA, A, BBB, C, D etc.) to countries based on their eco-political conditions

- India hold a credit rating in medium risk category just above the junk status

Also read: Capital Market – Equity

Factors affecting credit rating

- Fiscal deficit

- Inflation

- Infrastructure

- Foreign investment

- GDP growth

Bond vs Debenture

- Bond is the terminology used in England while debenture is the terminology used in America

- The term bond is used for a Government or PSU security while the term debenture is used for private companies securities

- In India, Bondholders are secured by access to the underlying asset in case of default by the issuer.

- Debentures, on the other hand, are unsecured, with debenture holders not having recourse to assets in the case of default by the debenture issuer.

Optionally fully-convertible debentures (OFCD)

- Investors have option to change Debentures to Shares

- If debentures are changed to shares then from companies point of view

- No further interest payment headache

- No profit to the company > No share

- Will only share dividend when company makes profit

- If debentures are changed to shares then from investors point of view

- If company makes higher profit

- He will get bigger dividend

Other Types of Debentures

- Non-Convertible debentures

- Partially convertible debentures > 100 Debenture – Rs. 70 (Non-convertible) + Rs. 30 ( Can be converted to Equity)

- Fully convertible debentures > 100 Debenture > Fully converted to equity (No Choice)

- Optionally convertible debentures > Choice after two years > For ex. 1 Debenture = 3 shares

- Redeemable vs irredeemable before Maturity period

- Fixed interest rate vs Index-linked interest rate (Sensex etc.)

Inflation Indexed Bonds – Primary Market Operations

Interest Rate: Real vs. Nominal

Why Gold consumption bad?

- Saving from Gold is not being used for capital expansion

- Gold import high > Trade deficit high

- Current Account Deficit increases > Rupee value decreases > Crude oil price increases

- Crude oil price increases > Petrol, Diesel price increases > Inflation increases

- Real Interest rate becomes even more (negative) > More Gold consumption

- This vicious cycle continues > Leading state to hyperinflation

- Can not ban Gold import ban > Leads to smuggling

- Solution > Provide new investment avenues with positive REAL interest rate

Inflation Indexed Bonds

- Inflation Indexed Bonds works on the principle of WPI Inflation Rate + X % Profit

- Compounded half yearly & can be traded at secondary market viz. from one investor to the other

| IIB (Inflation indexed bonds) | IINSS-C (Inflation Indexed National Savings Securities-Cumulative) |

|

|

|

|

|

|

|

|

|

|

Inflation indexed bonds losing shine

- Mutual funds invested heavily in IIBs during high inflation period

- But WPI is falling gradually since 2015

- Hence net interest rate of IIB stands out near 4 %

- Hence players exiting the game.

Credit Default Swap

- Insurance policy on bonds paying a certain premium

- When company defaults & even on liquidation can’t recover the money than insurance company will pay the investor.

For more updates, visit www.iasmania.com. Please share your thoughts and comments.

If you’re passionate about building a successful blogging website, check out this helpful guide at Coding Tag – How to Start a Successful Blog. It offers practical steps and expert tips to kickstart your blogging journey!

2 comments

Excellent article and very helpful

very helpful content. thankyou!