Monetary Policy & Inflation

Points to Ponder in This Article – This is the most important article in one’s upsc economy preparation. Read each and every word of this article with utter concentration to understand the nuance of economic system. Data given in this article may have changed over time but the basics remain same. Hence, read this article from head to toe as the most important one.

| Inflation | Rise in Prices | Not Good |

| Deflation | Fall in prices | Not Good |

| Disinflation / Creeping Inflation | Slow Rate of Inflation | Good |

| Stagflation / Misery Index | Stagnation + Inflation → Prices rise + No new Jobs | Not Good |

| Reflation | Policy to stop deflation without causing inflation | Good |

| Galloping Inflation | Inflation increasing in AP or GP | Not Good |

| Hyper / Runaway Inflation | Inflation averaging 100% in 3 years | Not Good |

| Recession | Decline in GDP for two or more consecutive quarters | Not Good |

| Depression | An extreme recession that lasts two or more years | Not Good |

| Core Inflation | Underlying inflation (Judged primarily by mfg sector) | Depends |

| Headline inflation | Core inflation + inflation in primary article (food + fuel) | Depends |

Sterilization

A form of monetary action in which a central bank seeks to limit the effect of inflows and outflows of capital on the money supply. Sterilization most frequently involves the purchase or sale of financial assets by a central bank and is designed to offset the effect of foreign exchange intervention.

Core sector India

- The eight core sector industries in India are — Coal, Crude oil, Natural gas, Refinery products, Fertilizer, Steel, Cement and Electricity

- Core sector contributes 38 % in the overall industrial production; a parameter that RBI takes into account while framing its monetary policy

Also read: Financial intermediaries – Banks in India

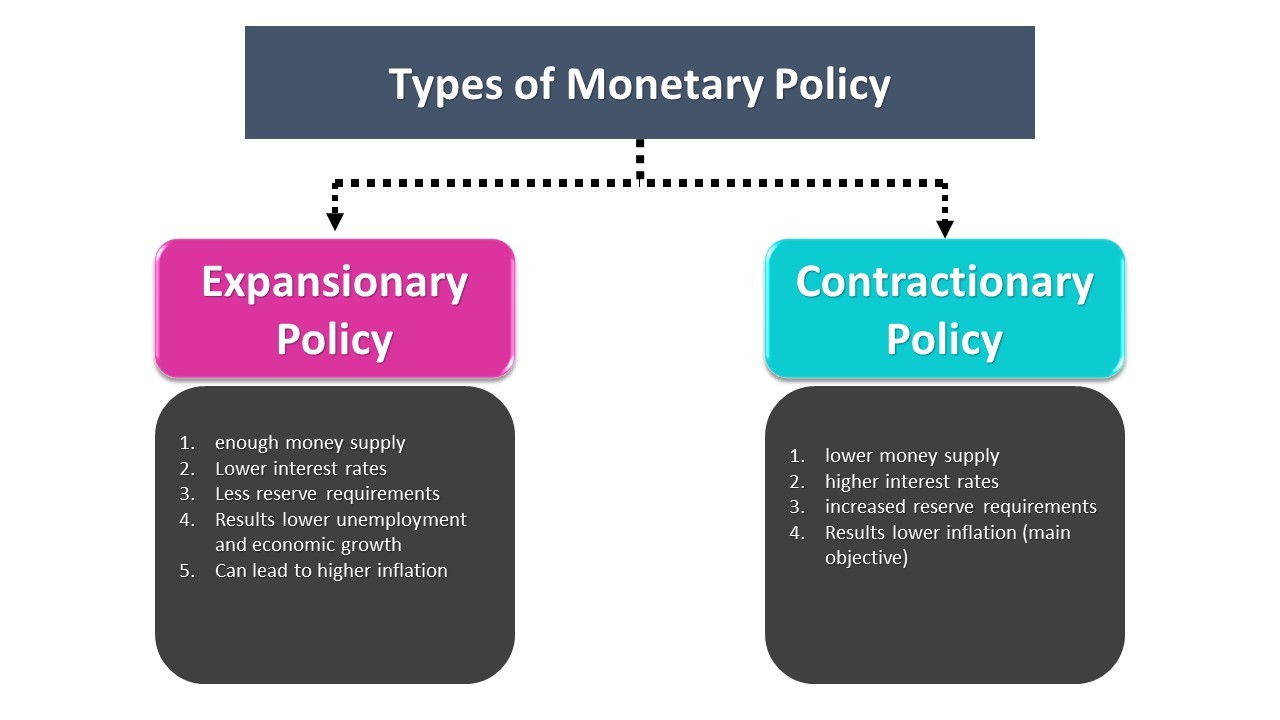

Monetary policy

- Policy made by Reserve Bank of India to check inflation or deflation viz. to control money supply in system.

- General fundamentals to check inflation or deflation > Control Money supply in system is –

To Combat Inflation

|

To Combat Deflation

|

Major Tools Used by RBI to Control the Money Supply

Quantitative, General, Indirect Tools

|

Qualitative, Selective, Direct Tools

|

Quantitative, General, Indirect Tools to Control Monetary Policy

Reserve Ratios > Cash Reserve Ratio (4%) + Statutory Liquid Ratio (21.5%)

- To protect your bank against the bank run (When everyone is rushing to take out money from bank)

- Stated in bimonthly monetary policy review

- Always counted on Demand & Time Liabilities

SLR (Statuary Liquidity Ratio)

- A Bank has to put 21.5 % of total money (Demand & Time Liabilities) with RBI in form of gold, cash or government securities.

- On Government securities bank also gets interest

CRR (Cash Reserve ratio)

- A bank has to set aside 4% of total money (Demand & Time Liabilities) with RBI in form of cash.

- No interest gain to bank

Net Demand & Time Liabilities

- On a particular day, depositors deposited 150 cr in bank & customers took out 50 cr from bank.

- NDTL > 100 cr > Reserve ratios will be counted on 100 cr.

- CRR (4%) > 4 cr cash kept aside for no use whatsoever > Levied on all banks > No profit to bank

- SLR (21.5%) > Cash, Gold, RBI approved securities (G Sec, Blue chip company shares etc.) > 5 cr > Levied on all banks > Profit to bank > Government securities (8%), Bonds, Shares may fetch profit, Gold reserves may fetch profit

- Bank left with 74.5 cr to lend to customers > further classification of this amount in PSL & commercial lending

- NDTL > Calculated fortnightly every second Friday

Demand Liabilities

- Current Account (CA)

- Savings Account (SA)

- Demand Draft

Time liabilities

- Fixed deposits (FD)

- Recurring deposits (RD)

- Cash certificates

- Staff security deposits e.g. bond in companies

Time liabilities > Demand liabilities as

- Current account fetches 0 % interest

- Saving account fetches 4-6-8 % interest

- FD/RD fetches 9% interest

Open Market Operations (OMO)

- When RBI starts buying or selling government securities in open market to control money supply

- RBI selling government securities > Less money with banks (as they invested in government securities) > Inflation reduced

- RBI buying government securities > More money with banks (as they sold government securities) > Deflation reduced

Rates > LAF (Repo Rate, Reverse Repo Rate), MSF, Bank Rate

Liquidity Adjustment facility (LAF)

Repo Rate (6.75% at Present) – Policy Rate

- If client borrows money from RBI (for short term – Even overnight) then client has to pay a fixed interest rate to RBI.

- Collateral > Securities other than of CRR & SLR

- Inbuilt clause of automatic re-purchase after a certain period as decided.

- Client being Central & State Gov., All banks & NBFI

Also read: Financial Institutions in India

Reverse Repo Rate (5.75 % at Present)

- If client lends money to RBI (for short term – Even overnight) then RBI has to pay a fixed interest rate to client.

- Collateral > Securities other than of CRR & SLR

- Inbuilt clause of automatic re-purchase after a certain period as decided.

| Repo Rate – 1%> Reverse Repo Rate | Repo Rate + 1% > MSF |

Marginal Standing Facility (MSF) – 7.75 % at Present

- Minimum 1 cr loan against 5 cr minimum in case of LAF

- Only scheduled commercial banks can borrow under this window (SBI, PNB, BOB, ICICI etc.)

- Banks Can use securities from SLR quota

- Maximum credit of 2% of net time & demand liabilities

Bank Rate (7.75 % at Present)

- When banks borrow long term loans from RBI, they’ve to pay a fixed interest rate to RBI

- No Collateral > Bank can borrow money without pledging government securities to RBI

- Bank rate is linked with penal rates viz.

- If CRR, SLR not maintained

- Penalty > Bank rate + 3%

- For repeat offender > Bank rate + 5%

- Bank Rate increased > Less money with banks > Inflation reduced

- Bank Rate decreased > More money with banks > Deflation reduced

Qualitative, Selective, Direct Tools to Control Monetary Policy

Loan to Value

- LTV = Loan/ Value of asset purchased

- Asset acts as a collateral

- If LTV is 75% & asset value is Rs. 100 then one will get only 75 Rs. against asset.

Margin Requirement

- Minimum margin required in hand to get a loan

- For e.g. Margin required is 75% then one can get only 25% loan.

“Increase Margin Requirement or Decrease LTV > Less money to borrower > Less Demand for product > Inflation reduced”

Consumer credit regulation

- RBI rule that minimum down-payment shall be x to get 1-x loan from the bank with monthly EMI minimum Y.

- Down payment or EMI increased > Product demand decreased > Inflation reduced

Selective credit control

- RBI specifically instruct bankers not to give loans to traders of certain commodities viz. sugar, Gur, edible oil etc. even if the said trader is ready to mortgage anything

- To prevents speculations / hoarding of commodities using money borrowed from banks

Rationing

- Putting a ceiling on total loans in each sector

- An example of planned economy

- Example > PSL target of 40% of NDTL

Priority Sector Lending (PSL)

- RBI instruction to all domestic banks & foreign banks in India to lend at-least 40% of their NDTL to priority sectors

- Foreign banks with < 20 Branches > 40% rule applicable but in phased manner from 2015 to 2019

- Priority sectors > Agriculture, Education, Housing, Export, Micro & Small Industries, RIDF etc.

If PSL targets are not met by banks then –

- Indian & foreign banks with 20 branches or more –

- Provide remaining money to RIDF (Rural infra. Development fund) managed by NABARD

- Provide loans to state governments for infrastructure development

- Bank earns interest + Principal

- foreign banks with < 20 branches

- Provide remaining money to SEDF (Small enterprises development fund) managed by SIDBI

- Lending to state industrial financial corporation

- Bank earns interest + Principal

Limitations of Monetary policy – No quick Results

- People don’t have many investment alternatives other than FD, LIC, Saving Accounts & PF

- Banks have large deposits from main supplier i.e. Public money (RBI is not a prominent supplier of money to banks)

- Whatever RBI does, its effect will be felt only after 6-8 months but by that time, new factors would cause another rise in inflation

- Lack of financial inclusion > People relying on moneylenders & barter system of transaction > Unorganized money market

- Monsoon uncertainty, cyclone, flood, draughts > Supply side constrains > Food inflation

- Crude + Gold import > Weaken Rupee

- Other Factors > Fiscal deficit, Subsidy leakage, Black money, Corruption

For more updates, visit www.iasmania.com. Please share your thoughts and comments.

If you’re passionate about building a successful blogging website, check out this helpful guide at Coding Tag – How to Start a Successful Blog. It offers practical steps and expert tips to kickstart your blogging journey!

3 comments

Excellent Post

Thanks ,for the standard notes. This is directly helpful for those who can not afford the coaching classes. Great move for the inclusive approach of online assistance.

Fantastic notes.. I like the approach making notes of economics and other subject as well… thanks sir